Your Favorite Vendors May be Headed for a Sale

Interest rates are finally dipping, so private equity is finally buying and selling tech companies again. Plus: The coming collision between AI and ESG, and two suggestions for mitigating it.

Private equity has been stuck in something of a logjam in recent years.

Starting in about 2022, fear of a possible recession, uncertainty about global unrest, and—above all—doubt about how long high interest rates would stay high have combined to produce a prolonged drought in exit activity. IPOs and acquisitions both hinge on confidence about economic conditions, and investors have had little to base decision-making on lately beyond gazing into a crystal ball.

“That’s really hard if you’re going to bet $50 million or $100 million on that crystal ball,” observes Barrett Kingsriter, senior managing director and founder of Pinecrest Capital Partners.

The upshot has been a lot of PE funds holding onto a lot of vendors for a lot longer than they normally would, and relying on continuation funds and “junk debt” to cash out the pension funds, insurance companies, and other institutional investors that capitalize them.

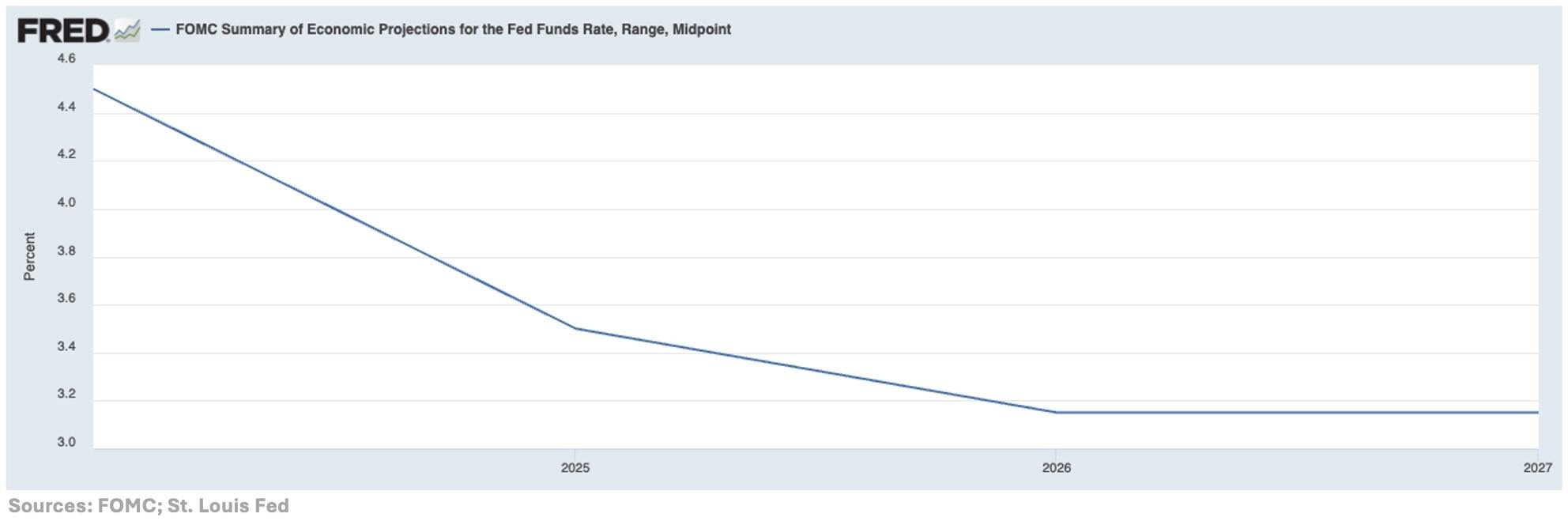

A bit worrying, but perhaps finally headed for the rearview mirror too now that interest rates, as we all know, have finally begun inching downward and the Federal reserve expects them to keep dropping well into the future:

The result in recent months, per new data from Pitchbook, has been the first increase in exits since 2021:

“The logjam is clearing,” Kingsriter says.

It’ll clear further and more rapidly going forward, he continues, barring prolonged war in the middle east, say, or a banking crisis of some kind.

“Absent that, I think there’s a 99% chance we see a material increase in deal volume in 2025,” Kingsriter predicts. “There’s a lot more comfort in putting capital to work.”

Not to mention a lot of accumulated capital looking for things to do, some $2.62 trillion of it according to S&P Global and more according to others. Not all of that money is headed for tech companies, but a lot of it is.

“There are still a lot of companies that are doing good things, building great technology, and being financially disciplined, and that actually deserve to be invested in,” says Chad Cardenas, founder and CEO of strategic capital investor The Syndicate Group.

Subscription-based software companies should do especially well, Kingsriter (pictured) adds. Economic indicators may be broadly encouraging, but there are still legitimate reasons to worry about a recession. In circumstances like that, investors look for acquisition targets with predictable recurring revenue streams.

“The SaaS world in general is going to be in favor,” Kingsriter says.

Look in the mirror. Are you smiling about all this?

Probably if you’re a PE firm with aging portfolio holdings and impatient investment partners, or a SaaS startup founder eager to fund further growth. Not so much, perhaps, if you’re one of the many MSPs who regard private equity with dread. Particularly because while larger, more mature vendors may begin testing the IPO waters next year, according to Kingsriter, much of the forthcoming deal activity is likely to involve PE firms selling vendors upstream to even bigger PE firms.

“I would expect to see larger private equity acquiring from mid-tier to smaller private equity really step up in 2025,” he says. “That’s where we’ve seen the pullback in M&A.”

Which is to say that like it or not there’s change coming to the vendor world and a lot of it is going to involve big-time private equity.

Personally, I’d discourage MSPs from regarding this as cause for panic. PE firms can and do shift budgets from support to sales and cut R&D spending. They also can and do accelerate product roadmaps and grow partner success teams. Better to train a wary eye and open mind on an acquirer than to bail out immediately should a massive investor buy your favorite vendor from a merely big one.

“It’s always important, or it should be at least, for channel partners to look at the attractiveness of a vendor relationship,” Cardenas says. “They look at the tech obviously, and the people, and the value proposition to the clients, and the use cases, and you go down the list of all the boxes you want to check, but then they also have to look at long-term viability of the company.”

Who owns the company should absolutely be part of that assessment as acquisitions heat up in the months ahead. So, however, should be what that owner actually does with their investment versus what you fear they might.

When AI and ESG collide

Stay with me on this one, folks, because I promise it comes around to vendors and their partners.

I live and work a bit less than a mile from the home of Seattle’s NHL and WNBA franchises, a facility that for the last three years has been named Amazon Climate Pledge Arena in honor of an initiative the tech giant co-founded late in 2019 to fight global warming.

To date, HP, HPE, Microsoft, Palo Alto, Salesforce, and 520 other companies have joined Amazon as signatories to the pledge, and I applaud them all. I also, however, increasingly wonder how confident they are about reaching their goal of achieving net zero carbon emissions by 2040. Amazon announced the Climate Pledge, after all, just a little over three years before the debut of ChatGPT, and with it generative AI.

Global spending on AI has soared since then on its way to a projected $631 billion in 2028, according to IDC, which expects AI-related data center energy use to grow at a 44.7% CAGR through 2027 to 146.2 Terawatt hours (TWh). How much is 146.2 TWh? A little over half of the U.K.’s entire electricity production in 2023 and about 4.6 times Ireland’s output, per the International Energy Agency.

All that additional energy consumption portends bad things for global carbon emissions. How bad, however, remains a mystery.

“I don’t think anyone is completely in agreement as to exactly what that impact is,” says Elsa Nightingale (pictured), principal ESG analyst at Canalys. “I fear, and I think many experts fear, it’s in fact much worse than we’d initially imagined.”0

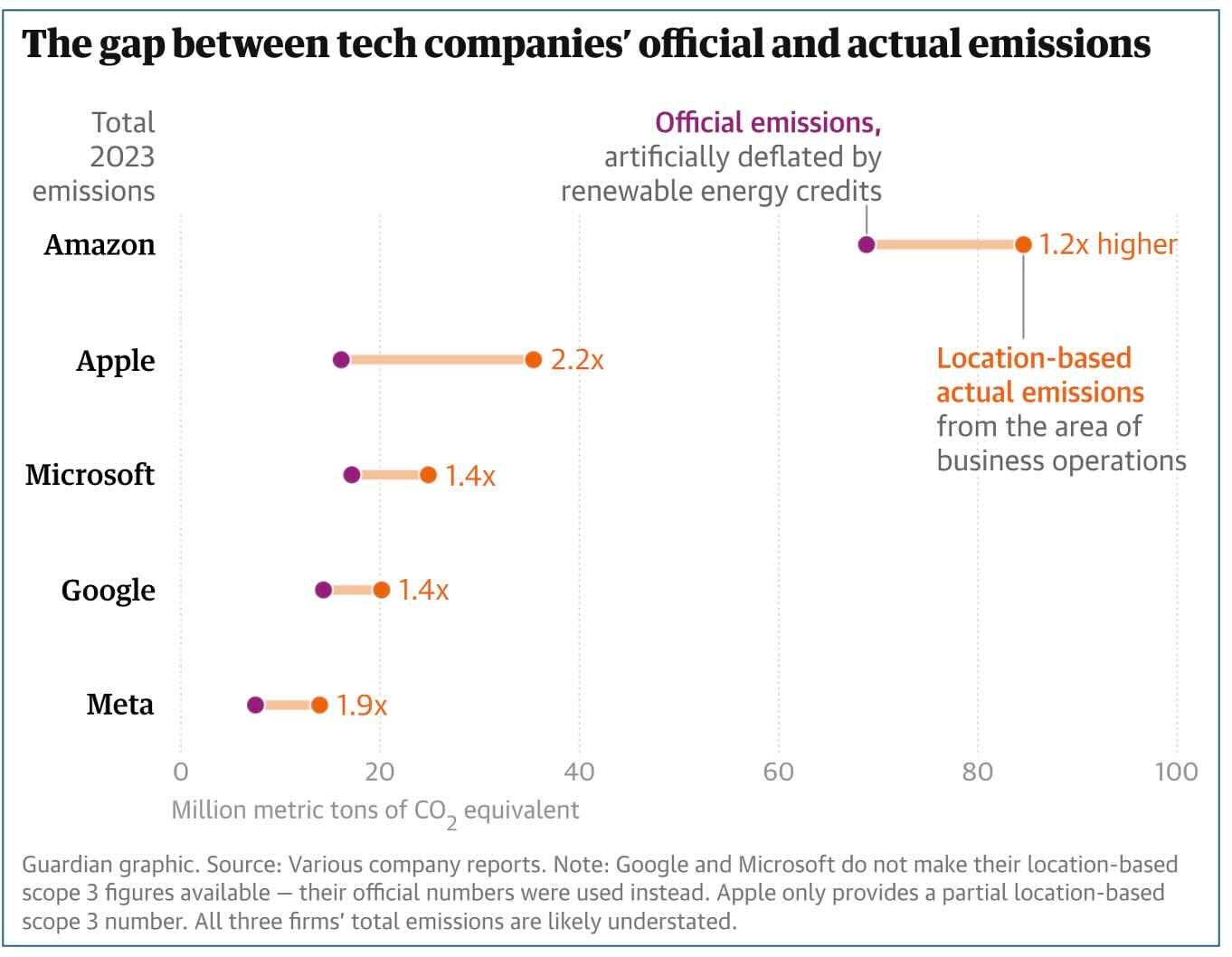

Google’s 2024 Environmental Report offers some clues. On the face of it, the numbers look good. Yes, electricity consumption rose 16.2% year over year in 2023, but that’s actually a slower increase than the prior year’s 19.1% uptick despite a whole lot of data center expansions. Similarly, while greenhouse gas (GHG) emissions rose 13.5% last year versus 2022, that too is better than the 17.1% increase recorded the year before.

On the other hand, those 2023 emissions were 48% above Google’s net-zero baseline measurement in 2019. And lest anyone accuse me of picking on Google, I’ll note that Amazon’s latest emissions are 34.5% above its 2019 baseline and Microsoft’s are 40.4% above a 2020 baseline.

Most of those increases, moreover, came before the AI explosion made further progress significantly harder, a fact of life that Google itself confirms in its sustainability report:

“As we further integrate AI into our products, reducing emissions may be challenging due to increasing energy demands from the greater intensity of AI compute, and the emissions associated with the expected increases in our technical infrastructure investment.”

Read further, moreover, and you’ll come across this bit about how Google is coping with that challenge:

“Starting in 2023, we’re no longer maintaining operational carbon neutrality. We’re instead focusing on accelerating an array of carbon solutions and partnerships that will help us work toward our net-zero goal, and are aiming to play an important role in advancing the development and deployment of nature-based and technology-based carbon removal solutions required to mitigate climate change.”

More specifically, Google is buying “high-quality carbon removal credits,” which is to say renewable energy certificates, or RECs. Loosely speaking, RECs document the purchase of electricity from a clean, emissions-free energy producer, and in theory they incentivize construction of more green power infrastructure. In reality, according to Nightingale, there’s little evidence to support that proposition, and because it’s perfectly legitimate to buy them thousands of miles from where your data centers are pumping out GHGs, RECs can make your actual environmental impact look better than it really is, per this recent analysis by The Guardian.

“Certificates are really problematic,” Nightingale says.

They’re also just one of the ways AI giants use or hope to use reporting rules to make sustainability metrics harder for partners and end users to assess. “Accounting really matters here,” Nightingale says.

Which gets us to the channel implications of this story. Per my last post on this topic a year ago, more and more businesses are embracing sustainability targets, thanks largely to proliferating compliance mandates. AI-related emissions growth, however, is on a collision course with those targets, and Nightingale suspects AWS, Google, and Microsoft won’t bear the brunt of the repercussions.

“Vendors will always be looked to as having the absolute responsibility because they own manufacturing, design, etc.,” she says. And because most of what vendors sell, especially to SMBs, passes through the channel, partners will be held accountable as well. That’s a tough spot to be in for both vendors and partners, because there’s only so much either can do about the problem beyond shoulder the blame.

Two ideas on AI and emissions

HP has a suggestion for mitigating the issue, and not surprisingly it involves AI PCs. Manufacturers measure power consumption by the NPUs in those devices in milliwatts, versus watts for CPUs, notes Guayente Sanmartin, HP’s senior vice president and division president for commercial systems and displays solutions. “This means the AI PC, for the workloads that you run in the NPU, are much more efficient from an energy consumption point of view,” she says.

HP’s units include AI-powered predictive maintenance functionality that expands their lifespan too, adds Alex Thatcher, the company’s senior director of AI experiences. “We talk a lot about power consumption, but the big heavy hitter for sustainability is making a device more usable or getting it to live across multiple users,” he says.

We’ll never check AI’s impact on ESG unless LLM operators chip in too, though. I learned about a vendor trying to help them do so this week. Called Multiverse Computing, the company uses techniques borrowed from quantum computing to compact AI models by over 90%.

“This means that you end up with a model using less than 10% of the memory than the original,” observes co-founder and chief scientific officer Román Orús (pictured), resulting in less than half the energy consumption. Quantum- and AI-based solutions like that are the only way out of the environmental mess artificial intelligence is otherwise sure to create, he adds.

“They are not an option; they are a must,” Orús says

Amazon, as it happens, appears to agree. The company hosted an invite-only genAI startup accelerator this week at its headquarters complex, which is even closer to my home office than the sports arena named after its climate pledge. One of the attendees was Multiverse’s CEO.

In his own words

You read about IT By Design CEO Sunny Kaila’s case for why MSPs should offshore some of their labor here a few weeks ago. You can hear him make the case himself on the new episode of the podcast I co-host. Available now wherever finer podcasts are distributed!

Also worth noting

Kaseya has launched a multimillion dollar effort to be fully FedRAMP authorized, and named Jon DePerro its vice president of FedRAMP and compliance solutions.

The Secure By Design pledge momentum continues. This week it was ConnectWise signing on.

The 20 (who you know well by now) has bought iCoreIT, the managed IT services division of publicly traded iCoreConnect.

Based on tech acquired along with Coveware earlier this year, Veeam Recon Scanner aims to help users proactively identify, triage, and prevent cyberattacks.

ConnectSecure has shipped an MSP-friendly vulnerability management solution for Microsoft 365.

Darktrace’s cloud detection and response solution now supports Microsoft Azure.

Malwarebytes unit ThreatDown has integrated its Nebula and OneView platforms with Google Chronicle SIEM.

NetApp has integrated unified data storage and intelligent services into the Google Distributed Cloud architecture.

Eaton has new enclosures purpose-built for big, heavy genAI data center hardware.

Wildix has introduced x-bees, an AI-powered, Salesforce-integrated system that blends voice, video, messaging, and conferencing into a single interface.